by Brian Shilhavy

Editor, Health Impact News

Will AppleID Become National Digital ID?

Who needs CBDCs or a National Digital ID program to track every financial transaction you make, when Apple has already beat everyone to the punch with their AppleID that now can be linked to your bank account as well?

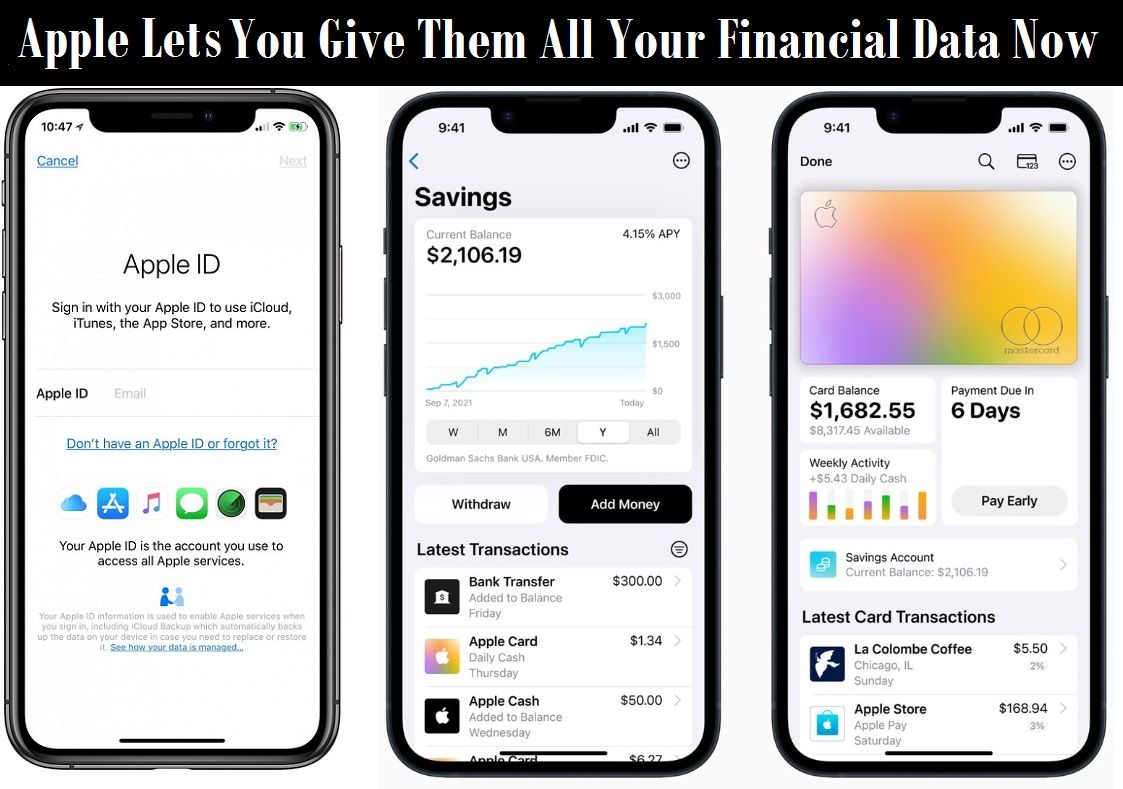

Yesterday, Apple announced that they are now offering attractive rates on savings accounts through their Apple Wallet, as they team up with banking giant Goldman Sachs.

With Elon Musk and others racing to create the first “do everything” app that can track pretty much everything one does in life, Apple just beat everyone to the punch by effectively making the iPhone, which is already in the hands of over 120 million people in the U.S., and over 1 billion worldwide, a device that can now pretty much link everything you do to your AppleID.

Apple is now paying you to have an iPhone!

That’s right. Sign up for the savings account now available through Apple Wallet, administered by Goldman Sachs, and you will get an interest rate of 4.15%, Apple announced today.

That’s a very good rate—most other digital-only banks aren’t offering terms quite as generous (as for big banks, forget it—their savings rates are still in the 0.01% ballpark).

Even Goldman Sachs, which actually operates the account, offers only 3.9% on its own Marcus savings accounts right now. Apple is presumably subsidizing that generous rate given that the account is for users of Apple cards, which means it’s designed mainly for iPhones and iPads.

It’s a smart way to entrench the iPhone even more deeply into people’s lives—smart for Apple, that is.

Whether this is smart for consumers depends on whether you’re comfortable having your life ruined if someone steals your iPhone.

The Wall Street Journal recently published an excellent report about how iPhone thieves are draining people’s bank accounts. That’s a result of people storing credit cards on Apple Pay and very often keeping photos of sensitive personal documents—passports and drivers’ licenses, for example—on their phones.

Some people even write down their passwords in the Notes app on the phone. When you stop to think about it, storing all this stuff on a phone does seem kind of crazy. (Full article – Subscription needed.)

This is a brilliant move by Goldman Sachs, which like all U.S. banks right now, is seeing a mass exodus of deposits since the banking crisis started last month.

In their first quarter report today, Goldman Sachs CEO David Solomon admitted that this partnership with Apple will increase bank deposits for their troubled bank.

Asked about Goldman’s new savings account with 4.15% interest for Apple Inc.’s Apple Card customers, Solomon said the business will open up Goldman’s deposit base without much overlap with its existing savings-account customer base. (Source.)

iPhone Users are Now Muppets

Pam Martens of Wall Street on Parade also covered this new venture today, reminding everyone how Goldman Sachs is part of the criminal banking cartel with their history of “dubious dealings” going all the way back to the Wall Street financial crash of 1929.

Apple Is Loaning Its Brand to the Great Vampire Squid to Offer FDIC-Insured Savings Accounts

Apple, maker of the iPhone and one of the top brands in the world, has decided to get deeper in bed with Goldman Sachs, a Wall Street trading house with more than 100 years of ignominious history.

Goldman Sachs was infamously branded as “a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money” by Matt Taibbi in the pages of Rolling Stone.

Of all things to offer through Goldman Sachs, Apple thinks it’s a swell idea to offer a high-yielding, FDIC-insured savings account – that is ultimately backstopped by the U.S. taxpayer if Goldman Sachs blows up – which it came close to doing in 2008.

Apple’s credit card is already offered through Goldman Sachs.

In an SEC filing on February 24, Goldman Sachs acknowledged that its credit card division is under federal investigation. A check at the complaint database of the Consumer Financial Protection Bureau (CFPB), a federal agency, shows that hundreds of consumer complaints have been filed against the Goldman Sachs/Apple credit card.

Among the hundreds of complaints filed at the CFPB is the following from a resident of Nevada. The complaint was filed on February 8 of this year: (Redacted material was done by the CFPB.)

“Late last year, Apple credit card pulled a hard inquiry on my credit and issued me an Apple credit card.

I did not request this credit card, so I contacted XXXX about this matter. Apple credit card closed my account and stated to me that they noted my account was closed because they could not verify that I requested, authorized, or applied for this credit card.

[…]

Pingback: Apple Turns iPhone into Ultimate Tracking Tool by Offering Banking Services – AppleID to Become National Digital ID? — The Most Revolutionary Act | Vermont Folk Troth